what percentage of american households give to charity dave ramsey

thirteen Min Read | Mar ten, 2022

If yous've never budgeted earlier—or you're wondering how your spending compares with anybody else'due south—you might wish you lot could come across some recommended budget percentages, national spending averages, and other helpful stuff like that all in one place.

Hey! This is that place!

And listen, nosotros aren't about to give you a i-size-fits-all budget per centum guide. Because your life isn't one size fits all! How much y'all should spend on this and that in your upkeep can vary depending on your income, household, location, goals, lifestyle—then many things.

Just there are a few standards to follow. Then, we've pulled them together with other helpful info to guide you lot equally you're setting up (or fixing upwards) your upkeep! Are you prepare for this? (Yes.)

Here. We. Get.

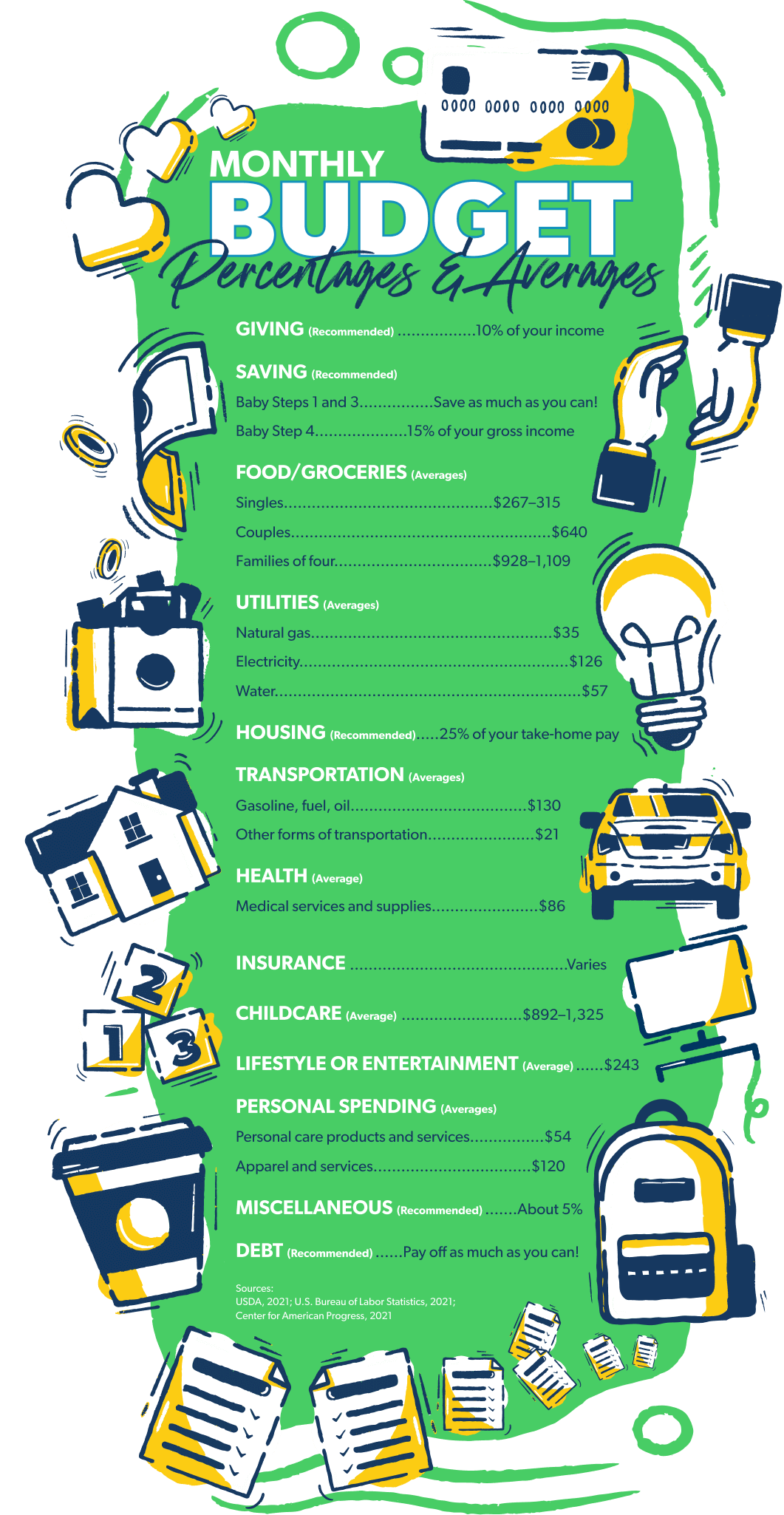

Guidelines for Setting Your Budget Percentages

Allow'due south break downwards some national averages and upkeep percent recommendations for common budget categories and upkeep lines.

Commencement budgeting with EveryDollar today!

If those words are new to you, remember of a budget category as a binder, and the upkeep lines equally files inside information technology. Or possibly a category is similar a playlist, and the lines are like songs. (Hm . . . perchance you should make a good money playlist to get you lot in the budgeting mood.)

And one more matter: If you're reading this as y'all set up your first budget, don't stop with the numbers we give y'all. Look up your own! Open your online banking company account or exit those bank statements and see what your past spending reveals.

Giving

We believe in giving. Always. Tithing to your church, donating to charities, supporting worthy causes—even if you're in debt. Generosity shifts the focus off of us (our problems, our fiscal shortcomings) and reminds the states of our blessings. Giving is good for you and for others, and nosotros recommend giving ten% of your income.

Saving

Heads up: You're about to hear us mention the vii Babe Steps. A lot. This is the proven, guided path to save money, pay off debt, and build wealth. (Aka how to win with coin.)

If you're wondering what's typical here, the average American saves around ix% of their income.ane But this is a neat instance of how a percentage or even an average shouldn't set a standard for you. How much you're putting in savings each calendar month depends on several factors!

When it comes to the savings category of your budget, think most these iii reasons to salve: emergencies, large purchases and wealth building. Since budget percentages for these tin vary, let'southward talk through each one.

Emergencies: Fix aside $one,000 in the banking company right away. (We telephone call that a starter emergency fund, or Baby Step 1.) This puts a greenbacks buffer between you lot and those life happens moments. If you've got debt (which we cover later) go along that emergency fund at $1,000 until you're debt-free (which is Baby Footstep 2).

When the debt'due south gone, you need to save up what we phone call a fully-funded emergency fund (Baby Stride 3). This is 3 to half dozen months of expenses and will protect y'all against bigger emergencies, like job loss or your automobile going kaput.

It'due south hard to tell you lot what per centum of your income to put toward your emergency fund. Basically, if you lot don't have i yet, you need to cut dorsum on whatever extras and go intense on stuffing cash into your savings until yous practice!

Large Purchases: Some other reason to put money in savings is if you lot're planning whatever big purchases. This includes saving up for a reliable car to supercede the one y'all know is on its last legs (er . . . final tires?).

The key word here is know. When your machine breaks down, to your consummate surprise, that's a job for the emergency fund. But when yous know your beater is hanging on by duct tape and prayer, that's when you start saving for a replacement.

Habitation repairs work the aforementioned way, really. Some are surprises. Some aren't. So, go on your optics on your stuff and so you'll know when to put money in savings for those necessary big purchases.

What nigh the fun big purchases? Like vacations, new furniture or that boat to make all your fishing dreams come true? You lot should salvage upwardly greenbacks for these too! Simply get to the luxuries subsequently you're debt-gratuitous and take some solid financial security. (The boat can await!)

Again, in that location isn't a gear up pct here. Just remember—the more coin you throw at a goal, the quicker you get in that location!

Wealth Building: The final reason to save up money is forwealth edifice. Once you've paid off your debt and are sitting on top of that fully funded emergency fund, it's time to kickoff saving for the hereafter!

This time, we accept a solid percent for y'all: At this stage of the game, you should exist investing 15% of your gross income for retirement savings.

Pro tip: Larn more nearly walking the 7 Baby Steps.

Food

Eating in, eating out. When nosotros're not making or consuming food, we're thinking almost nutrient, correct? It'south no wonder this upkeep line is one of the hardest to wrangle.

While we don't take a set percent here, we tin give you lot some national averages of what Americans spend on groceries each month in the "moderate" spending range:2

- Singles historic period xix–50 spend $267 to $315.

- Couples age 19–50 spend $640.

- Families of four spend between $928 and $1,109.

What about restaurant spending? The average per household is $2,375 a year (around $198 a month if you divide it equally).3

As y'all start budgeting, these numbers might assist—but know that the size of your family unit, any dietary restrictions, and your lifestyle will all affect your spending here.

As yous budget from month to calendar month, pay attending to what you plan versus what you lot commonly spend. Are you over upkeep? Why? Information technology could be that your expectations are unreasonable—or that your spending is! Both can be fixed. You'll just need to work at it.

Pro tip: Go the Rachel Cruze Meal Planner and Grocery Savings Guide.

Utilities

Utilities

The utilities budget category includes electricity, h2o, natural gas or propane, and trash services. These all can vary based on where you live and how many people you live with!

Here are some helpful stats—the average "consumer units" (similar to households) spend:4

- $414 a year (about $35 a month) on natural gas

- $1,516 a year (well-nigh $126 a calendar month) on electricity

- $682 a year (about $57 a month) on water

Pro tip: Larn how to salve money on your electric nib.

Housing

Housing (or Shelter) should exist no more than 25% of your have-home pay. This includes your rent or mortgage paymentsplustax, insurance, HOA fees and private mortgage insurance.

And so, when you're crunching numbers to see if y'all tin afford that lavish flat complex with a pool, pet spa and playground—call back 25%. When you're plugging totals into the Mortgage Calculator to see if the neighborhood of your dreams would actually become the monthly payment of your nightmares—remember 25%.

(Besides, remember these numbers: fifteen-year stock-still and x–20% down. They'll aid yous when you're house hunting.)

Spending anything over 25% a calendar month on your housing will make the rest of your upkeep percentages tight and can turn what's meant to exist one of your greatest blessings—your home—into a financial burden.

P.S. This per centum will change when you're on Baby Step 6, which is all about paying off that home early. When y'all're mortgage-gratis, you lot won't have to worry about putting 25% toward housing anymore! All that money tin go to living (and giving) like no one else!

Pro tip: Learn how to salve on domicile expenses.

Transportation

Gasoline, car tag renewals, oil changes—it all adds up. This category volition vary depending on where you lot live, whether you have a long commute to and from work, what you lot bulldoze, and whether you have access to bang-up public transportation. On average, American households in 2020 spent:5

- $1,568 on gasoline, other fuels and oil (just over $130 a month)

- $263 on other forms of transportation (just over $21 a month)

Pro tip: Learn how to save money on gas.

Wellness

Wellness

This category is an excellent example of how percentages can change from calendar month to calendar month or year to year.

If you lot go to the optometrist to update your glasses prescription, or you fall off the stage while performing inMacbeth and literally break a leg, you'll spend more on your health that month than the next month when you're only fine. If your kid needs braces, that's a couple years of college health expenses.

On average, American households in 2020 spent $1,034 total (about $86 a calendar month) on medical services and supplies.6

Pro tip: Save money on things your wellness insurance doesn't encompass.

Insurance

Though insurance isn't fun to talk virtually or spend money on—it is a must. No matter where you are with your money goals or Baby Steps, these iv types of insurance are essential: health, home, car and term life.

We as well recommend identity theft protection, long-term inability insurance, umbrella/liability insurance (if you've got a net worth of at to the lowest degree half a 1000000 dollars), and long-term care insurance (if y'all're 60+).

All of these vary based on, well, a ton of different things like your historic period, previous health concerns, the kind of car you drive, your personal driving history, the size and location of your dwelling, your assets, and the list goes on and on.

The best thing you can do here is take our Coverage Checkup. You tin can make sure you lot've got the coverage yous need—and not more than. (Yeah, crazy, but some people are over-paying and over-covering!) You lot'll also get an action plan for whatever insurance you're missing.

Childcare

With childcare, we're talking about making a budget category to comprehend whatever expenses needed for parents to work—not the extra babysitting money for date nights. (That can go under the amusement category, which we'll talk virtually next!)

The average cost of childcare ranges from $ten,700 to $15,900 a year per child (most $892 to $ane,325 per month).7 Of class, this varies based on where you live, the kind of childcare you pick, and how many kids you take!

Pro tip: Learn more than on how to budget for childcare.

Lifestyle or Entertainment

If you want to buy tickets to meet your favorite boy ring perform with the local symphony, yous'll need a lifestyle (or amusement) category. The average American household spends $two,912 a year here—which is nigh $243 a month.8

But allow'due south be honest for a infinitesimal: If you lot're in debt or living paycheck to paycheck with zip in savings—cut out this budget category until yous've got financial security. Yeah, it sucks to say no to things for a season, but it's just a flavour. It'southward worth the sacrifice at present to get you to a better place with your coin in the future!

Personal Spending Money

The amount of personal money yous budget for each month depends on your income and Baby Stride. If you lot're saving upward an emergency fund or paying off debt, any fun money spending should strike this residual: It should be depression plenty to help you go to your goals quickly but only plenty to proceed you from falling off the budgeting carriage.

Looking dorsum at those national averages, American households spend $646 a year (virtually $54 a month) on things labeled equally "personal care products and services" and $one,434 (about $120 a calendar month) on "apparel and services."nine

And here's an of import callout on wearable: If you need clothes for growing kids who don't fit in their things anymore, that'southward dissimilar than wanting this season'southward latest and greatest because you love way. Wants like this should get nether personal spending and are covered after needs.

Miscellaneous

It'due south difficult to program for everything and still brand a zero-based budget—unless you create a miscellaneous category for about 5% of your have-home pay.

This is for the things that popular up in a month but aren't actual emergencies. You'll be prepare if your kid gets a last-infinitesimal invite to a friend'south birthday party. With a miscellaneous category, you can grab a gift without derailing your upkeep.

The miscellaneous category is also great for those times y'all underestimate how much yous'll need for a certain expense. Allow'due south say yous get the water bill, and it's a little more than expected. Merely motility some money from the miscellaneous category to the utilities category.

If you don't terminate up spending anything from your miscellaneous category, give yourself some high fives. (Okay, so that's mostly just clapping, only that works likewise.) Then put all that extra cash toward your current Baby Step!

Debt

If you've got debt, information technology'due south time to cut out extras, lower your spending, and look into ways to upwardly your income. All the extra coin y'all add together to the upkeep from doing these things should become to paying off your debt.

Nosotros aren't giving you a set percentage—we're saying throw everything you can at this super of import coin goal.

Because the affair is, debt robs this month'southward income to pay off the past. You can't go ahead when you're constantly paying for the by. So, complimentary up your paycheck (all of it) by getting debt out of your life. Pronto.

Pro tip: Use the debt snowball method to pay off your debt. Fast.

How Practise I Determine the Right Budget Percentages?

And then, it'south non about putting yourself inside this upkeep percent box with everyone else in the whole entire budgeting world. That. Doesn't. Work.

If y'all want to make a budget that does piece of work (for you—in your stage of life, with your income, Baby Step and money goals in heed), our all-time slice of advice is to check out Ramsey+.

Okay, cool cool—only how will Ramsey+ aid yous budget? Well, start a gratis trial, and and then get watch Budgeting That Actually Works. In 5 brusk lessons y'all'll learn how to gear up up a budget that fits where you are and so you lot can get to where y'all want to be!

And so put the lessons in action by downloading the premium version of our budgeting tool, EveryDollar. Premium means features like depository financial institution connectivity (which makes tracking your transactions throughout the month simple and authentic) and budget reports (which bear witness you your spending and income trends).

The truth is, it doesn't thing if y'all've budgeted never or a million times—you can do it with confidence. Starting right at present. Call up about the numbers we've shared hither, look at your ain numbers, start that free trial to Ramsey+, and become your coin working equally hard equally you practice.

About the author

Ramsey Solutions

gillisonnevency99.blogspot.com

Source: https://www.ramseysolutions.com/budgeting/budget-percentages